The Ultimate Guide to Ecommerce Sales Tax

Tim is a Certified QuickBooks Time (formerly TSheets) Pro, QuickBooks ProAdvisor, and CPA with 25 years of experience. He brings his expertise to Fit Small Business’saccountingcontent.

Meaghan has provided content and guidance for indie retailers as the editor for a number of retail publications and a speaker at trade shows. She is Fit Small Business’s authority onretailand ecommerce.

This article is part of a larger series onRetail Management.

Ecommerce sales tax is a type of consumption tax that online merchants collect from customers and then pass on to the government. Also referred to as online sales tax, it is charged as a percentage, though the specific amount changes depending on the merchant’s and customer’s locations.

It works a bit differently when selling online as opposed to selling in a physical store because you’re doing business in multiple states, so it’s important to get familiar with how ecommerce tax works and what you need to do to be compliant.

Luckily, most ecommerce platforms and online store builders, includingShopifyandBigCommerce, automate sales tax collection based on your business information and the information customers enter at checkout, so there’s no manual calculations needed.

How Ecommerce Sales Tax Works

销售税总是指控的比例total sale. Each state sets its own percentage, as well as parameters around which goods are eligible for sales tax. Some states add sales tax to everything, while others add it to nothing. And others still apply sales tax to some items and not to others. The rules change depending on the state and sometimes local jurisdictions override state rules with their own.

Selling online makes sales tax a bit tricker because your location is less straightforward. Your business’s headquarters might be in one state, with warehouses in another. And your customer base could be all over the country—or the world.

当政府看着在线商家的sales tax, it considers the business’s connection to each state, or “sales tax nexus.” We will discusssales tax nexusin more detail below, but it includes any state where you have a physical presence and may include where your customers are located and other business activities that tie you to a specific state.

This wasn’t always the case though. A few years ago, online merchants were only required to pay ecommerce sales tax to states where they have a physical presence.

Physical presence:A store, office, warehouse or other business facility as defined by the state

But the 2018 South Dakota vs Wayfair Supreme Court ruling changed that. Now, businesses with sales exceeding more than 200 transactions or $100,000 in in-state sales must collect and remit sales taxes to that state, even if they don’t have a physical presence there. Since the ruling, 45 states and Washington D.C. have implemented their own ecommerce tax laws.

States also get to choose the following sales tax factors:

- Physical presence: States can decide which business activities qualify as a “physical presence.”

- Economic threshold: States can impose higher transaction rates or gross sales amounts. Some states use only the in-state revenue and don’t count transaction rates.

- Additional taxes: Several states have local sales taxes, which are added on top of the state sales tax.

- Sales tax sourcing: States can choose whether they’re an “origin-based” or “destination-based” sales taxing source. Origin-based means states impose ecommerce sales tax based on where the business originated, while destination-based uses where the product is shipped. Most states are destination-based.

- Marketplace facilitator: Several states have passed marketplace facilitator laws requiring third-party marketplace sites like Etsy or Amazon to collect and remit sales tax with each sale.

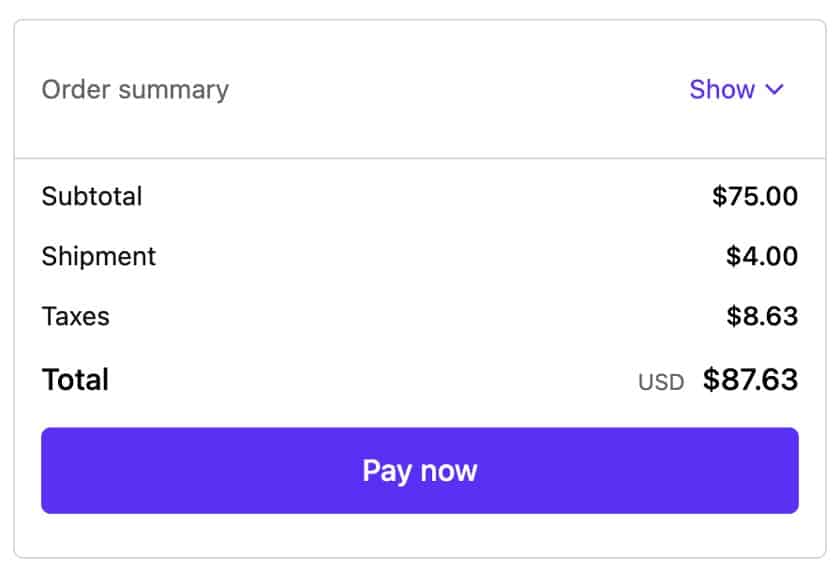

When a customer comes to your online store and makes a purchase, your checkout will automatically calculate the necessary sales tax based on the customer’s shipping and billing information. This tax is an additional line item and added to the total cost of the transaction.

In thisShop Payexample, the total cost for the products is $75 while the taxes are calculated at $8.63.

When to Charge Ecommerce Sales Tax

You’re responsible for sales tax if you sell a taxable product or service in a state where you have a sales tax nexus. If you qualify, you’ll need to collect and remit the taxes back to the appropriate state.

What Is a Sales Tax Nexus?

如果你的在线商店进行一定量的business in a particular state, it will trigger tax obligations, creating a sales tax nexus. You’llalwaysqualify for a sales tax nexus in your business’s home state. But you might also qualify in other states as well.

The following business activities may create a nexus:

- Owning or renting a physical space: An office, warehouse, storage facility, store, or home office creates a presence in the state.

- Staff: Having an employee, contractor, salesperson, or other personnel in a state may create a nexus.

- Inventory: Storing inventory in a warehouse or through other third-party fulfillment centers likeFulfillment by Amazoncould prompt tax responsibilities.

- Click-through nexus: Some states have laws regarding third-party affiliates and sales tax obligations.

- Temporary locations: Retail businesses that have a short-term physical business in a state, such aspop-up shops,trade shows, or craft fairs, can be required to collect sales tax.

- Economic threshold: If your business exceeds a specific dollar amount in sales or a certain number of transactions to customers located within a state, you might need to collect and remit taxes to the state.

Ecommerce Sales Tax Requirements by State

Expand the sections below for a list of the states that currently impose ecommerce sales tax. It’s always best to consult your local jurisdiction directly for the latest information and to confirm additional details.

Alabama: 8%

Alabama’s Department of Revenuestates that online retailers have a nexus if they have a physical presence such as a retail store, warehouse, inventory, or regular visits of traveling salespeople, or has aremote entity nexus. Alabama is a destination state.

Alaska: 0%

Alaskadoesn’t have a state sales tax, but it does allow local municipal governments to implement a sales tax. The charges are destination-based if the retailer qualifies for a nexus.

Arizona: 5.6%

Arizona’s Transaction Privilege Tax (TPT)is a tax on the vendor for the privilege of doing business in the state. Vendors must collect and remit payment back to the state. Arizona is an origin state for sellers with a nexus. Arizona also allows local municipalities to set their own ecommerce sales tax rates.

Arkansas: 6.5%

All remote sellers and marketplace facilitators must collect and remit sales tax to theState of Arkansaswhen selling tangible personal property, taxable services, a digital code, or specified digital products for delivery exceeding $100,000 or 200 transactions within the current or previous year. Arkansas is a destination state.

California: 7.25%

Californiarequires all remote sellers to collect tax if the total combined sales of tangible personal property for delivery in California exceeds $500,000 during the previous or current year. Districts can also add a tax if they want. California’s sourcing is mixed, which means that city, county, or state taxes are based on the seller’s location, while district taxes are destination-based.

Colorado: 2.9%

Coloradomandates retailers to obtain a sales tax license if sales exceed $100,000 in a year. Colorado is a destination state. Colorado also allows local municipalities to add an ecommerce sales tax.

Connecticut: 6.35%

InConnecticut, if you make at least 200 retail sales into the state and at least $100,000 in gross receipts from sales, you’ll need to pay ecommerce sales tax. Marketplace facilitators also need a permit if they had more than $250,000 in sales the previous year. Connecticut is a destination state.

Delaware: 0%

Delawareis one of five states without a sales tax. However, some online merchants may have to pay a Gross Receipts Tax. In Delaware, wholesale transactions are destination-based while retail sales are “based on the passage of the title within Delaware.”

Florida: 6% + 0.5%–2% Discretionary Tax

If you’re out of state but make more than $100,000 in total sales from Florida customers, you’ll need to register and collect, report, and remitFlorida sales taxand discretionary sales surtax. Florida is a destination state.

Georgia: 4%

Out-of-state merchants and marketplace facilitators inGeorgianeed to collect ecommerce sales tax if they gross more than $250,000 per year or process more than 200 transactions in the previous or current calendar year. Georgia is a destination state.

Hawaii: 0.5%, 4%, 4.5%

Hawaiihas aGeneral Excise Tax (GET)instead of a sales tax. GET is a tax on businesses rather than the customers, but merchants have the right to pass it on to shoppers. The type of business activity determines rates. The general GET rate in Hawaii is 4% (4.5% in some counties) but it’s 0.5% for wholesaling goods, manufacturing, and some other business activities. Merchants need to pay a one-time $20 fee to register for GET.

Idaho: 6%

Idahorequires you register for a state seller’s permit and pay ecommerce sales tax, or use tax, if your Idaho sales or Idaho third-party sales exceed $100,000 in a year. If you use a marketplace facilitator, then you’ll also have to pay ecommerce sales tax should your annual sales exceed $100,000. Note that you’ll need a separate permit for your direct sales and marketplace facilitator sales. Idaho is a destination state.

Illinois: 6.25%

Illinois requiresremote retailers or marketplace facilitators making at least $100,000 in sales or processing at least 200 transactions in the state to pay ecommerce sales tax. Illinois is an origin state if your business is located within it. If you’re not an in-state seller, then you’re considered destination-based.

Indiana: 7%

Any remote retailer that processes 200 or more separate transactions or grosses more than $100,000 in a year inIndianawill have to pay sales tax to the state. You can register via theStreamlined Sales Tax Registration Systemor withINBiz. Indiana is a destination state.

Iowa: 6% + Optional 1% Local Option Sales Tax (LOST)

Iowarequires any remote seller that earns $100,000 per year in gross revenue or processes more than 200 transactions for sales into Iowa in a single year must collect and remit sales tax. You’ll need to register for a sales tax permit with the state, either through the Streamlined Sales Tax Registration System or Iowa Department of Revenue’sBusiness Tax Registration System. Iowa is a destination state.

Kansas: 6.5%

Kansasrequires any retailer that makes more than $100,000 from sales to customers in the state to pay ecommerce sales tax. Kansas is a destination state.

Kentucky: 6%

Out-of-state remote sellers who make more than 200 sales intoKentuckyor $100,000 in gross receipts from sales must register and collect sales and use tax. Kentucky is a destination state.

Louisiana: 8.45%

Louisianarequires ecommerce businesses to charge a Consumer Use Tax for all customers located in the state. Merchants can either pay annually or report and pay viaConsumer Use Tax Return, Form R-1035. Louisiana is a destination state.

Maine: 5.5%

Mainerequires sales tax from any business that sells tangible personal property, products transferred electronically, or taxable services to customers in the state. Businesses that make 200 or more sales or earn more than $100,000 from sales in a year are also required to register and collect sales tax. Maine is a destination state.

Maryland: 6%

Marylandcharges a flat statewide use tax rate of 6% on most goods and increases that to 9% for alcohol purchases. The items must be used or intended for use within the state. Maryland also has two tax-free events each year. Maryland is a destination state.

Massachusetts: 6.25%

Online merchants will owe ecommerce sales tax toMassachusettsif they make at least $100,000 in sales to customers in the state in a single year. If eligible, you’ll need toregister with the Department of Revenue (DOR). Massachusetts is a destination state.

Michigan: 6% Sales Tax + 6% Use Tax

Michiganrequires any business that exceeds $100,000 per year in gross revenue or makes more than 200 transactions in the previous or current year to collect and pay asales tax of 6% as well as a 6% use tax. Michigan is a destination state.

Minnesota: 6.875%

Minnesotarequires qualifying ecommerce merchants to collect and remit sales tax. Marketplace sellers don’t need to remit sales tax to the state of Minnesota because the respective marketplace does so. Minnesota has what it calls the Small Seller Exception. The Small Seller Exception means sellers who make less than $100,000 or process fewer than 200 transactions for purchases made by Minnesota customers do not have to pay sales tax. If you exceed this threshold, you’ll need to notify Minnesota within 60 days. Minnesota is a destination state.

Mississippi: 7%

Mississippi指控一个基于总销售和使用税s of sales or gross income. Merchants need apermit or registration license from the Department of Revenuebefore they collect sales tax. Mississippi is an origin state.

Missouri: 4.225%

Missouri’s Department of Revenuestates that any sales to customers in the state should collect and pay sales and use tax. Cities and counties may also add their own additional taxes. Missouri is an origin state.

Montana: 0%

Montanais one of the few states that doesn’t charge a sales tax or an ecommerce-specific sales tax.

Nebraska: 5.5%

Nebraskarequires sales and use tax from online merchants earning $100,000 per year in gross revenue or making more than 200 transactions in the previous or current calendar year. City and county governments can also choose to tack on an additional sales and use tax at 0.5%, 1%, 1.5%, 1.75%, or 2%. Nebraska is a destination state.

Nevada: 4.6%

Remote sellers inNevada也受到100000美元和200 transacti吗ons threshold. The state offers the option to volunteer to register and collect the tax as a “benefit to their Nevada customers.” Local jurisdictions can add their own sales and use tax. Delivery charges are not taxable. Nevada is a destination state.

New Hampshire: 0%

New Hampshiredoesn’t charge a sales tax or an ecommerce-specific sales tax.

New Jersey: 6.625%

Similar to other states,New Jerseyfollows the $100,000 sales and 200 transactions per year limit. New Jersey gives merchants a 30-day grace period after they’ve met the threshold. New Jersey is a destination state.

New Mexico: 5.125%

New Mexico has aGross Receipts Tax(GRT) rather than a sales tax, and businesses will have to pay rates based on where the products or services are delivered. New Mexico is an origin state.

New York: 4%

New Yorkrequires all vendors that meet either their physical presence or economic threshold to pay sales tax. However, its economic threshold is different from other states. It requires vendors and marketplace facilitators that exceeded $500,000 and made more than 100 sales of tangible personal property delivered in the state during the “previous four tax quarters” to register as a sales tax vendor. New York City boroughs charge an additional 4.875% sales tax, which is the highest for the state. However, many other counties, such as Westchester, also charge additional sales tax. New York is a destination-based sales tax state.

North Carolina: 4.75%

Any remote retailer who meetsNorth Carolina’s thresholdof 200 or more separate transactions or earns gross revenue of more than $100,000 in North Carolina in the current or preceding calendar year will be required to collect and remit sales tax. Local municipalities also add a sales tax. North Carolina is a destination state.

North Dakota: 5%

InNorth Dakota, ecommerce retailers have to pay state sales tax as well as city and county taxes. The economic threshold is the standard $100,000 in retail sales into the state or 200 or more transactions in a year. North Dakota is a destination state.

Ohio: 5.75%

Ohiohas a standard sales and use tax, plus additional taxes that vary by county. All out-of-state sellers with at least $100,000 of retail sales into the state or more than 200 transactions in the current or previous calendar year need to pay the tax. New online business owners should apply for tax payments 30 days before launching their website. Ohio is an origin state.

Oklahoma: 4.5%

Oklahomarequires any remote seller that sells at least $100,000 worth of taxable items in the state during the current or previous year to collect sales tax from the customer. If remote sellers don’t meet the threshold, they must notify customers that a use tax must be paid by the customer unless the product is exempt. Local jurisdictions can also add a sales tax; in some places, the total sales tax reaches 11.5%. Oklahoma is a destination state.

Oregon: 0%

Oregondoesn’t charge a sales tax or an ecommerce-specific sales tax.

Pennsylvania: 6%

Pennsylvaniamandates online retailers and marketplace facilitators with annual gross sales greater than $100,000 to register, collect, and remit sales tax payments to the state. Local municipalities may also add a sales tax. Pennsylvania is an origin state.

Rhode Island: 7%

Any online retailer or marketplace facilitator with a sales nexus inRhode Islandmust pay sales and use tax. Like other states, the economic threshold is $100,000 in sales or 200 transactions in a year. Rhode Island is a destination state.

South Carolina: 6%

South Carolinarequires sales tax from ecommerce sellers with gross sales revenue exceeding $100,000 into the state in the previous or current calendar year. You’ll need a retail license to remit sales tax. Municipalities can also add on their own sales tax of up to 1%. South Carolina is a destination state.

South Dakota: 4.5%

Ecommerce businesses that exceed $100,000 in sales into the state or 200 transactions in the current or previous calendar year must pay sales tax inSouth Dakota. South Dakota is a destination state.

Tennessee: 7%

Tennesseerequires sales tax payments from any ecommerce business with at least $100,000 in sales to customers in the state in the previous 12-month period. Additional local tax rates vary by county or city. Tennessee is an origin state.

Texas: 6.25%

Texasallows remote sellers with less than $500,000 in sales for the prior year and without a physical presence in the state to choose to collect the alternate single local use tax rate instead of the total local tax rate. Local jurisdictions can also tack on additional sales taxes, but they can’t exceed 2%. Texas is an origin-based state.

Utah: 4.7%

InUtah, the state sales tax rate is 4.7%, and local jurisdictions may also choose to add their own. In some places in Utah, ecommerce sales tax rates can reach 8.7%. Like other states, online sellers with over 200 transactions or $100,000 in sales in the current or previous year must pay taxes to the state. You’ll need to register for a sales tax license through theTaxpayer Access Point, mailing or faxingform TC-69, Utah State Business and Tax Registration, or registering with theStreamlined Sales Tax member states. Utah is an origin state.

Vermont: 6%

Vermontrequires ecommerce businesses to pay sales tax if they generate over $100,000 of retail sales into the state or have at least 200 transactions in the current or previous calendar year. Vermont is a destination state.

Virginia: 5.3%

Ecommerce businesses must collect and remit sales tax to the state ofVirginiaif they sell more than $100,000 or process more than 200 transactions in the current or previous calendar year. Additional local sales taxes may also apply. Virginia is an origin state.

Washington: 6.5%

Washington Staterequires remote sellers and marketplace facilitators with more than $100,000 in sales to in-state customers in a year. You’ll need tofile a Business License Applicationto collect and remit sales tax. Resellers will also need a specificReseller permit. Washington is a destination state.

Washington D.C.: 6%

TheDistrict of Columbiaalso requires ecommerce sales tax from sellers with more than $100,000 in sales or more than 200 transactions in a year. Washington D.C. is a destination state.

West Virginia: 1%

InWest Virginia, local municipalities set ecommerce sales tax rules.Of the 43 that do, most charge 1% though some have a sales and use tax rate of 0.5%. The state mandates sales and use tax from online retailers and marketplace facilitators with more than $100,000 in sales or 200 transactions in a year. West Virginia is a destination state.

Wisconsin: 5%

Wisconsinrequires remote sellers and marketplace facilitators to pay sales tax if they have annual gross sales of more than $100,000 or if they have 200 or more retail transactions in the current or previous calendar year. Local jurisdictions also have the option to charge an additional tax;in most cases, this is 0.5%. Wisconsin is a destination state.

Wyoming: 4%

Like many other states,Wyomingrequires a state use tax from online sellers who process either at least 200 transactions or $100,000 in sales in a year. Wyoming is a destination state.

Ecommerce Sales Tax Requirements by Product

Ecommerce sales tax requirements for products vary by state. Most tangible personal property items and a variety of services are taxable; however, some states exempt certain products.

Exemptions include:

- Clothing: Most states tax clothing; however, several states have exceptions based on certain thresholds. Some states, like Connecticut, have a luxury tax on clothing and footwear priced over $1,000.

- Food and groceries:Thirteen of the 45 stateswith a sales tax stilltax groceriesat a reduced or full rate.

- Medications: Prescription drugs are almost alwaystax-exempt, but non-prescription and supplements are usually taxable items.

It’s also wise to periodicallycheck with your stateto ensure you tax your customers correctly.

How to Stay Compliant With Ecommerce Sales Tax

Register for Your Sales Tax Permit

Once you’ve determined that you have nexus with a particular state, you might need asales tax permitfor that state. Registering your business with the state’s taxing authority ensures compliance and will alleviate potential issues.

The specific steps to register for a permit vary by state, but generally, the process is as follows:

- Gather essential business documentation, like your employer identification number (EIN).

- Go to thestate’s tax agency website.

- Locate the “Sales and Use Tax” section—use “ecommerce” or “remote seller” as keywords for your search.

- Follow the steps to register your business.

Set Up Your Business’s Tech Platforms

Keeping up with the laws and regulations of each state can be difficult. Choosing the rightecommerce platformandaccounting softwareis important because many options automatically calculate ecommerce sales tax for you.

Prioritize platforms with settings to accurately and automatically calculate sales tax rates for each state where you have a nexus. Some programs, likeTaxJar, integrate with many popular ecommerce platforms and can calculate the sales tax, track your economic nexus threshold in each state, and automatically submit returns for multi-state filings.

Consider Wholesale & B2B Sales Tax Exemptions

If you plan onselling products wholesaleto other businesses, different sales tax rules may apply. Some states don’t require sales tax to be collected when you sell products to a business that will turn around and sell the product again. This is because, in the US, sales tax is only charged at the point of sale to the end customer.

确保所有的B2B客户索赔be exempt from sales tax withholding have the proper exemption form from the state. You might consider not accepting exemption certificates just to play it safe; resellers that do unnecessarily pay sales tax can usually apply for a refund from the state.

Learn more aboutwholesale sales tax.

Bottom Line

When you sell online, it’s important to keep up with current ecommerce sales tax rates and regulations in the states where your business, products, staff, and customers are located. Remote seller and marketplace facilitator laws will continue to evolve, so it’s important to integrate software and conduct occasional audits to ensure compliance.