40+ Payment Statistics for Small Businesses (2023 Edition)

Meaghan has provided content and guidance for indie retailers as the editor for a number of retail publications and a speaker at trade shows. She is Fit Small Business’s authority onretailand ecommerce.

Agatha Aviso is a writer of the Reviews Section at Fit Small Business, focusing on order fulfillment and eCommerce platforms. Agatha has a decade’s worth of experience writing online content for small businesses and marketing industries. She also served as a content strategist and digital marketing manager for many entrepreneurs.

This article is part of a larger series onPayments.

Learn payment statistics around consumer preferences for speed and convenience, including a decline in cash use and an increase in mobile and contactless payments.

New payment trends and technologies like buy now, pay later (BNPL) and innovations across traditional payment channels like live chat and messaging platforms have also mushroomed into the mainstream. Below, we review general customer payment preferences and payment statistics and trends across the retail, ecommerce, restaurant, and B2B industries.

Similar to our2022 Payment Trends Report, consumer payment preferences that started forming pre-pandemic accelerated during the COVID-19 pandemic and have cemented themselves as the norm. We see continued trends for an increase in contactless, mobile, and digital wallet payments over traditional tenders like cash.

Retailers have also stepped up and started implementing alternative payment methods (as well as emerging trends such as cryptocurrency), though data from the recent State of Retail Payments of the National Retail Federation (NRF) shows thatcredit cards are still the most usedpayment method by customers.

According to a Pew Research Center study, Americans areheading to a cashless economy.From 2019 to 2021,cash as an in-store payment method fellfrom 15% of all transactions to just 11%.

Cashless spending has become the norm for consumers, with 41% of Americans not using cash for their weekly purchases—compared to 24% in 2015 and 29% in 2018.

In fact, 69% of shoppersforesee a completely cashless future.

Cash usage alsovaries widely based on demographics.Age, income, and ethnicity show a role in cash preferences. Adults older than 50, households with less than $30,000 annual income, and Black consumers prefer to pay in cash.

Mobile wallet adoption has increased significantly since the second quarter of 2022, led mostly by Generation Z and millennial consumers. Gen Z consumers hadone in 10 mobile wallet transactions(a 29% increase from 2021). Millennials and bridge millennials paid for in-store purchases through mobile wallets 7.9% (44% growth) and 7.7% (31% growth) of the time, respectively.

Adoption rates across all income and financial lifestyle segments have also increased except for those earning $100,000 or more annually, which fell just below 6%.

While mobile wallets are still far from outpacing contactless cards as a payment preference of most consumers, they are themost popular new payment method—59% of consumers who tried a new payment method in the past year used one.

According to a PYMNTS.com report, less than 23% of surveyed consumers were interested in trying out a new payment method, except for one—digital wallets. Almost half arewilling to give digital wallets a tryin the next 12 months.

Tap to pay is winning the battle for touch-free checkouts. In the second quarter of 2022,contactless card paymentsaccounted for 14% of in-store purchases, 2.5 times more than mobile wallets and nearly twice the figure from 2021.

According to S&P Global Market Intelligence’s Connected Customer, Disruptive Technologies 2022 survey, almost three in five (59%) US customershave a contactless card.Over a third (34%) use it more often due to its tap-to-pay functionality.

We expect the increase in contactless payments to continue, with many card issuers still rolling out contactless cards to their customers and many merchants still lacking the technology to process them. A report by the American Bankers Association’s Contactless Economy projected that 87% ofdebit cards would be contactlessby the end of 2022.

Related:

- Learn more about theNFC payment technologythat powers contactless card payments and additionalcontactless payment statistics.

There is growing popularity of alternative payments among consumers, but the NRF sees mobile wallets or Buy Now, Pay Later (BNPL) options posing no danger to eclipse credit and debit card usage in the payments market.

For example, digital wallets, while increasingly popular, took up only2.6% of card payments, according to the Federal Reserve Board Publication. Apple Pay, which is used thrice as much as Google Pay, onlyaccounts for 2.4%of in-store purchases.

BNPL providers’ (Affirm, Afterpay, Klarna, PayPal, and Zip)$24 billion in purchasesfrom over 180 million consumers is still a far cry from the$9.4 trillion for credit and debit card purchasesin 2021, even if the revenue is a tenfold increase from 2019.

Learn more about BNPL:

The 2022retail and ecommerce payments trends report重申付款习惯转变期间形成的the COVID-19 pandemic are the new normal. Retailers and consumers quickly adopted contactless payment methods (like Apple Pay) and opted for alternate pickups (“buy online, pick up in-store,” curbside) during the pandemic.

Since then, digital payment options have only increased in popularity, and retailers are continuing to adopt alternative payment methods. Other payment methods like Buy Now, Pay Later (BNPL) have also seen rapid adoption because of increasing consumer awareness.

We also see fraud and security risks are still crucial in retailers’ payment decisions last year and will drive their priorities into 2023.

Retailers continue to implement various digital payments.Apple Pay and Google Pay are leadingthe pack, with 80% and 65% of retailers either offering or planning to implement the payment methods, respectively, in their stores within the next 18 months.

In the past three years, consumer awareness andadoption of BNPL has skyrocketed.Forrester’s 2022 data indicates 15% of US online adults have used Afterpay, Affirm, Klarna, PayPal Credit, or Pay in 4 (with PayPal) in the past three months to make a purchase.

Due to the increase in consumer demand, 58% of retailers who participated in the NRF Survey have alreadyimplemented at least one BNPL optionin-store, with 38% of retailers coming out with their own installment financing options.

Retailers remain wary of adoptingcryptocurrencyas a payment method for their stores, although there arebig brandsthat currently accept crypto—Chipotle, Regal Cinemas, Whole Foods Market, Baskin-Robbins, and GameStop.

In the NRF 2022 State of Retail Payments report, only 2% of respondentshave implemented Bitcoin or other cryptopayments in their stores. Moreover, nearly 65% of retailers do not expect their businesses to accept crypto in the next three to five years, citing a lack of consumer demand. Other reasons include regulatory uncertainty (59%), exchange rate volatility (42%), and risk and complexity issues with know your customer (KYC), and anti-money laundering (AML) (42%).

Mitigating fraud and reducing feestopped merchants’ payment priorities last year and will most likely continue in 2023.

In 2022, retailers’ top priorities were improving security and implementing new digital and mobile payment methods. The NRF report shows thatreducing fees from payment gateways(36%) dominated in-store payment initiatives. Supporting omnichannel settings ranked second. Fraud mitigation ranked third on the list, with chargeback reduction also a crucial priority for retailers, ranking fourth.

Fraud Mitigation

Forty-two percent of retailers said improving security (fraud, management encryption) is among their top three priorities, with 57% of respondents agreeing that requiring PINs improves transaction security (notably down from 71% in 2020 and 95% in 2018). Interest is growing in other areas—43% would implement biometrics for credit card transactions if banks allowed them (compared to 22% in 2020).

Fees Reduction

Fees remained a pain point for most retailers last year, with 30% of them saying the costs of accepting payments (like processing and network fees) were a top challenge in the past 12 months. Twenty-one percent said the same about chargebacks.

Ecommerce retail greatly benefited from the emergence of alternative payments, such as digital wallets. Whileshopping cart abandonment rates remain very high, BNPL and one-click checkout options are seen to help decrease abandonment rates.

It will be interesting to see online merchants’ current efforts to extend payment methods across traditional payment channels. Live chat, third-party messaging apps, and social commerce are top priorities for payment initiatives in 2023

当woul购物车遗弃d-be customers start an order on a website and then leave the items without purchasing, is a common pain point for businesses of all sizes. Abandonment rates slightly decreased from the end of 2021 through 2022, but overall abandonment rates remain very high. More shoppers abandon their carts than complete a purchase.

According to thelatest cart abandonment study, extra fees like shipping and taxes are the main reason for cart abandonment. However, a majority also leave their carts because of the checkout process—they don’t want to create an account to check out (24%), they don’t trust the website with their credit card information (18%), checkout was too long or complicated (17%), or there are not enough payment options available at checkout (9%).

To help decrease abandonment rates and increase conversions, streamlining the checkout process and adding more payment options are essential. For example, adding a BNPL payment option can help reduce sticker shock at checkout, as the amount customers pay at the point of purchase is much lower. Digital wallet payments and one-click checkout options mean shoppers don’t have to manually enter their card information or enter it at all.

Learn more aboutshopping cart abandonment rates and statistics.

Digital payments continue to be rolled out across ecommerce platforms, withApple Pay and PayPal leading the stakesonline: 78% and 74% of retailers already accept or have plans to implement those payment methods, respectively, on their websites in the next 18 months.

A smaller percentage of retailers currently accept P2P payments. Only 9% and 4% of retailers accept Venmo and Zelle payments, respectively, on their websites, and 15% and 13%, respectively, have plans to implement the two payment methods within the next 18 months.

One-click Checkout: Counterpart of Contactless Card Payments

Contactless payments have made accepting in-store payments faster and more convenient. Unfortunately, this convenience has not been brought online. With 64% of the respondents in the Mastercard New Payments Index (NPI) survey (from March–April 2022) saying they are likely to make anonline payment via the manual entry of card detailsover the next year, it is clearly time to have the benefits of tap-to-pay come to online clicks.

Enter the one-click checkout (OCC). This checkout option has slowly rolled out across popular ecommerce platforms in the past year. While there has been some resistance, with 70% of those surveyed expressing security concern, payment providers are quick to explain that OCC is different from card on file (CoF), where retailers save consumers’ cards on their database.

With one-click checkouts, consumers’ payment details are stored securely in the payment providers’ gateway through tokenization, similar to how NFC (or contactless) payments are secured.

According to C+R Research, around two in five people plan toreplace their credit cards with BNPL.总的来说,38%的消费者认为payment option will eventually replace their credit cards because it is easier to make payments (45%), more flexible (44%), and offers lower interest rates (36%).

Nearly half of online merchants havestarted offering BNPL checkout optionsin their ecommerce platforms, with more merchants planning to accept at least one BNPL solution in their online store in the next 18 months.

The NRF 2022 State of Payments report shows that today’s consumers want to be able topay for products across different devices, platforms, and channels. Retailers are stepping up to this challenge by implementing an optimized payment experience for smartphones (mobile commerce capabilities) and planning on accepting payments in conversational touchpoints (such as chatbots, SMS/mobile text messaging, and other third-party messaging platforms) and other innovative payment interfaces (like social commerce).

Customer preferences and restaurant priorities are still generally aligned, with both wanting faster, more convenient ordering and service options. Still, online ordering and online payment abilities top customer requests for technology features in restaurants, with fast-lane in-store pickup coming in a close second.

A PYMNTS Digital Divide study in October 2022 revealed that ordering channelsrequiring customers to visit the restaurant, such as dine-in and pickup, remain the most popular despite all the delivery options.

While the study shows in-person dining options remain the most popular, there is noticeable demand for alternative ordering options, calling out restaurants to offer more choices to fit consumers’ lifestyles. Overall, we see the restaurants that can offer the best omnichannel experience will have the most reach for customers.

A PYMNTS and Paytronix collaboration survey among US adults who regularly order food from restaurants shows that 40% of restaurant customers think online ordering or payment features could encourage them toplace more restaurant orders.Among technology requests, online ordering is the most popular (41%). Features related to pickup, like fast lane in-store pickup (39%) and drive-thru pickup (38%), are also among the top in the list.

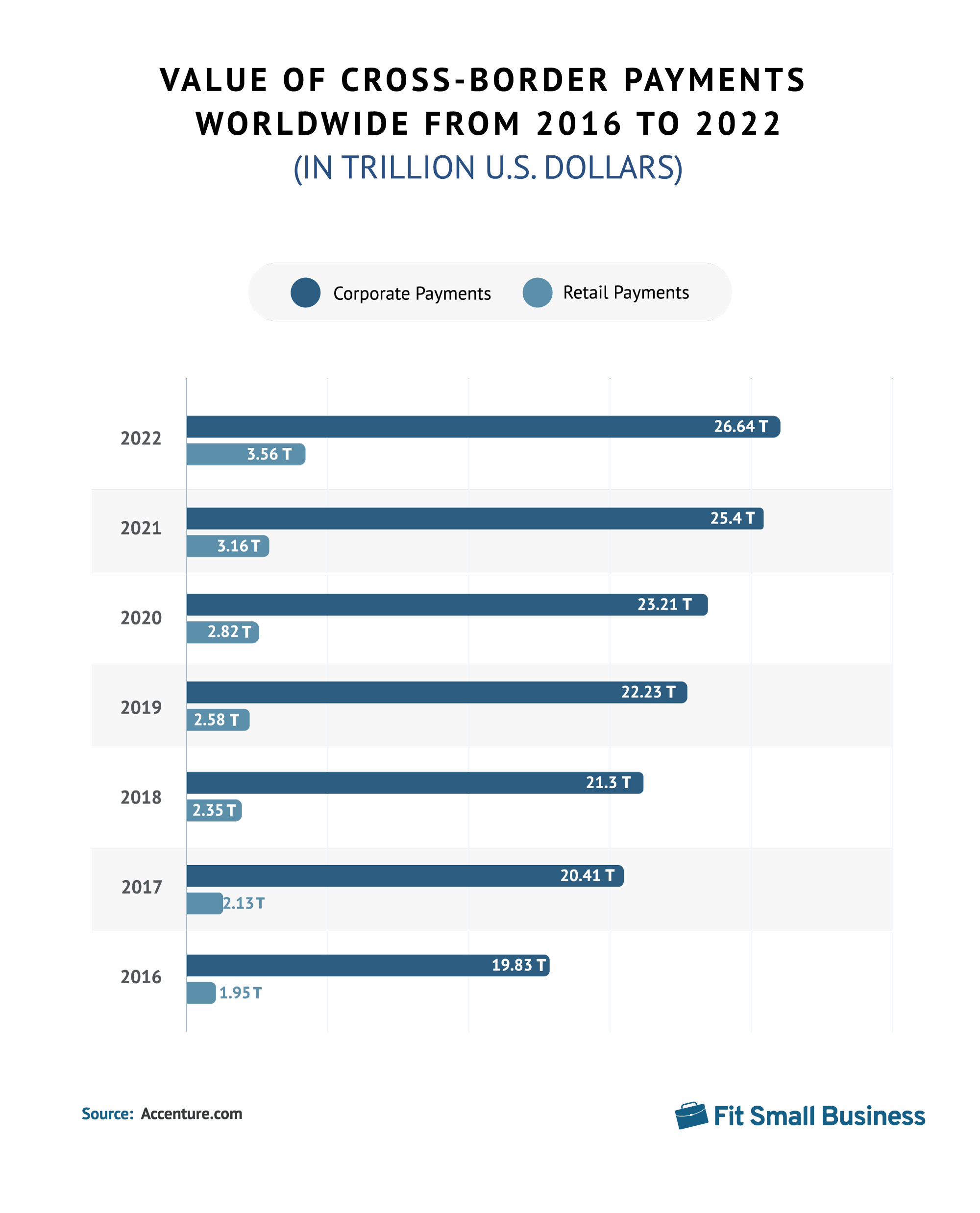

According to market analysis,B2B global transaction value will growby 26% between 2022 and 2027. By 2027, over $111 trillion in payments will be transacted globally, up from $88 trillion in 2022.

Despite beingthree times as largeas the B2C payment market, B2B payment technology infrastructure and adoption rates drastically lag behind B2C payments. Many B2B businesses are still being paid through traditional methods. Generally, 23% of B2B customers are stillrequired to pay in personwhile 22% pay over the phone. These outnumber those that are able to pay online or via an app (31%). Adopting B2C payment methods will significantly help increase efficiencies in B2B operations.

Learn more aboutB2B payment statistics and challenges.

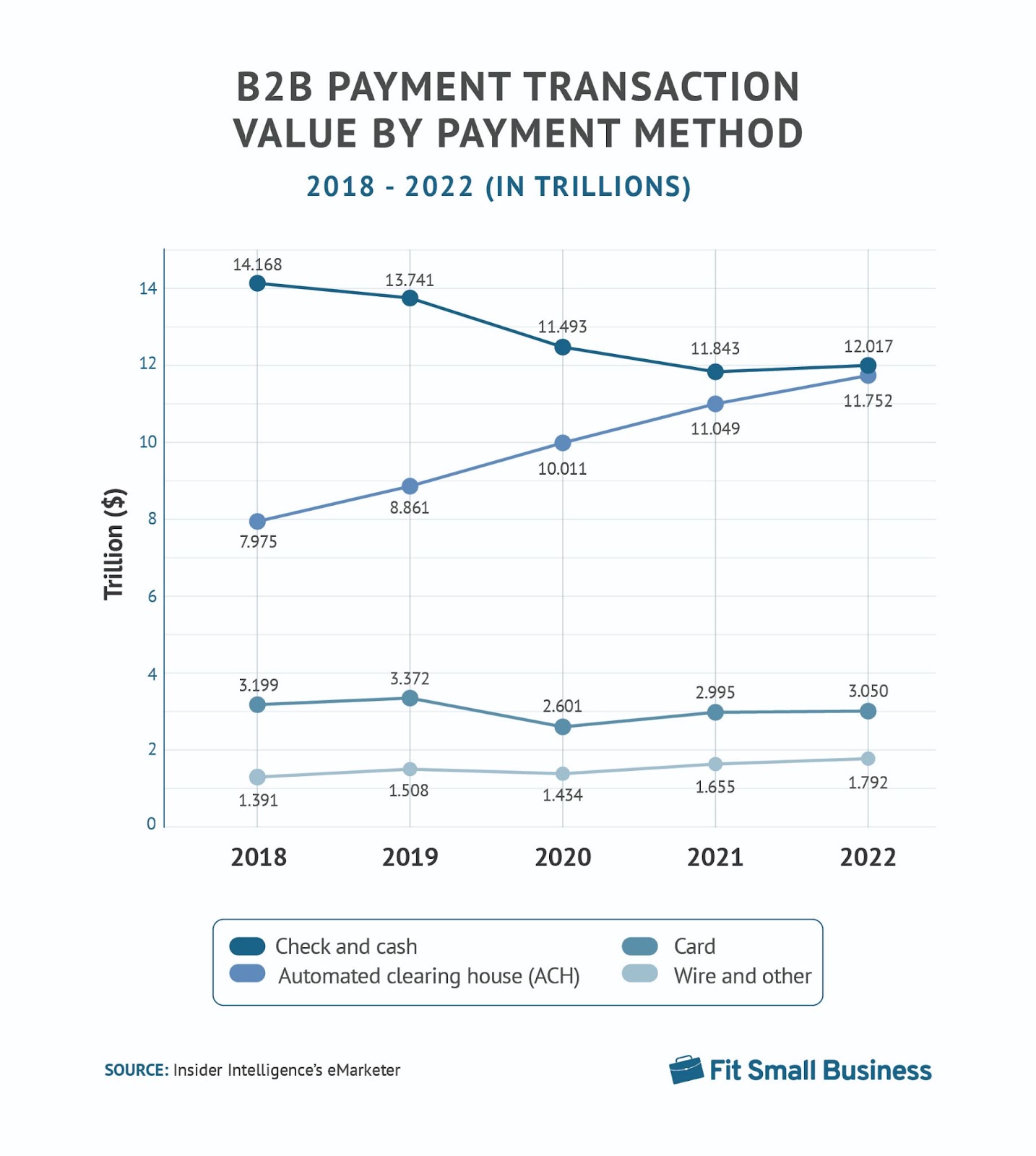

Insider Intelligence’s eMarketer estimated that US B2B payment transaction value wouldgrow 7.8% year over year (YoY) in 2022to $27.542 trillion, based on the above image.

According to a Blue Snap report, 68% of B2B businesses are potentiallypaying unnecessary cross-border feesby processing payments from international customers in the country where their business is located rather than where the customer is located.

Almost half (48%) of respondents estimate they’ve lost up to 10% of their international revenue because their payment processing vendors do not offer the right payment options. This is further confirmed by Flywire, as it saidcurrency fluctuations and FX rate are the biggest challengesin global market expansions, with 88% saying cross-border payment collection impacts business growth.

Did you know?

It takes businesses55% longer to receive cross-border paymentsthan domestic ones.

B2B cross-border payments should implement modern invoicing and billing solutions along with local card acquisition and support for local payments to mitigate revenue loss.

Bottom Line

Small businesses can appeal to customers and changing payment trends by choosing amerchant accountandpoint-of-sale (POS) systemthat enables contactless, digital wallets, and online payments.

Preferences for these payment types are not a passing fad; contactless payments and frictionless transactions are here to stay.