IRS Form 1099 Reporting for Small Businesses in 2023

This article is part of a larger series onHow to Do Payroll.

IRS Form 1099 is a series of forms used to report certain types of income that don’t come from a direct employer in the form of wages, salaries, tips, etc. Form 1099-NEC (nonemployee compensation) is the most common version, frequently used by small business owners.

If businesses pay $600 or more in compensation throughout the year to contractors, freelancers, or other nonemployees, they are required to send copies of Form 1099-NEC to the IRS and payees. (Before 2020, this was reported on 1099-MISC.) Form 1099-NEC is typically issued to individuals, sole proprietors, partnerships, and LLCs treated as either sole proprietorships or partnerships.

Form 1099-NEC is due Jan. 31, 2023, to report 2022 calendar year payments. You can print blank 1099-NEC form copies from the web or fully completed forms from your payroll software—many offer it for free.

What Is a Form 1099-NEC & When Is It Due?

Form 1099-NEC is an information return. Its primary purpose is to give nonemployees a record of the total annual payments they received and need to report during tax time (you won’t withhold or pay anyemployer taxeson the money you pay contractors). 1099-NEC forms also alert the IRS to who received untaxed payments throughout the year, just in case those individuals don’t self-report and pay their tax bill.

The due date for furnishing a copy to your contractors and vendors and filing a copy with the IRS is Jan. 31 for most businesses; however, when that date falls on a weekend, it’s due the following Monday.

As noted earlier, in prior years, contractor payments were included in Form 1099-MISC. If you need to file a 1099 for nonemployee income paid in 2019, you would use the2019 1099-MISC. We cover1099-MISC and other types of 1099 formsin more detail later in this article.

How to Prepare & File Form 1099-NEC in 4 Steps

Preparing and filing a Form 1099-NEC is relatively simple as long as you’ve kept good records. The form itself is brief.

Step 1: Have All Independent Contractors Complete a Form W-9

Before paying a contractor for any work, it is important to have them complete and sign aForm W-9. Form W-9 shows information you will need for preparing Form 1099-NEC, such as the contractor’s name, address, and taxpayer identification number.

Go through your records and find out if you need to request Form W-9. Store them with yourpayroll forms.

The links for downloading Form W-9 are:

- Form W-9: This is the blank Form W-9; have your contractors fill this out, sign it, and send you a copy.

- Instructions for the requester of Form W-9: These instructions are for businesses and cover issues such as when to ask for a Form W-9 from a contractor.

If you don’t want to worry about handling paper tax forms and also have W-2 employees, then you can use payroll software like Gusto to do it for you. Contractors enter their personal information on electronic W-9 forms that automatically transfer to year-end 1099 forms, so you don’t have to fill out anything—you can also use it to prepare W-2s for employees. These automations make it much easier to do payroll. Gusto even lets you pay independent contractors via direct deposit or check, all for $6 per worker each month they’re paid. Get started withGustotoday.

Step 2: Track Payments Made to Independent Contractors Throughout the Year

Businesses can monitor payments made to contractors and vendors manually or by using software. At the end of the year, compile a report showing the total amount of payments to each contractor. Analyze this report to determine which contractors you need to send a Form 1099-NEC to.

If you’re tracking payments manually, use Microsoft Excel or Google Sheets. You can enter formulas to automatically sum the payments, so you always have a running year-to-date total.

Step 3: Complete Form 1099-NEC at the End of the Year

一旦你有了一个报告显示总金额支付to each contractor and the Form W-9, you are in a position to prepare the Form 1099-NEC. Fill out the form for each contractor or vendor as required.

The different ways a business can prepare Form 1099-NEC include:

- Filling out paper forms:Order blank forms from the IRS for free; be sure to get Form 1096 in addition to Form 1099-NEC (Form 1096 is a summary of all the 1099 forms you issue and should be sent to the IRS alongside the 1099 copies). It’s important to note that all forms sent to the IRS must be machine readable forms in red ink. Forms cannot be printed to send via mail.

- Downloading PDF forms:Use the downloadable Form 1099-NEC to prepare the copy you send to contractors and vendors. Download the 2022 version of Form 1099-NEC from the IRS website, and then type in information on-screen and print.

- Using payroll software:If you prefer to file your Forms 1099, you will need to use software that can e-file the forms or work with someone who has access to tax software. Manypayroll softwarehave a feature contractors can use to print the completed form themselves, makingdoing payrollthat much simpler.

- Using accounting software:Some accounting software programs can prepare, print, and e-file Form 1099-NEC.

- Using Form 1099 software:There are a handful of desktop and web-based software programs for preparing and e-filing Form 1099.

- Hiring an accountant:You canhire an accountantor tax preparer to prepare and e-file your 1099 forms in addition to your income tax return.

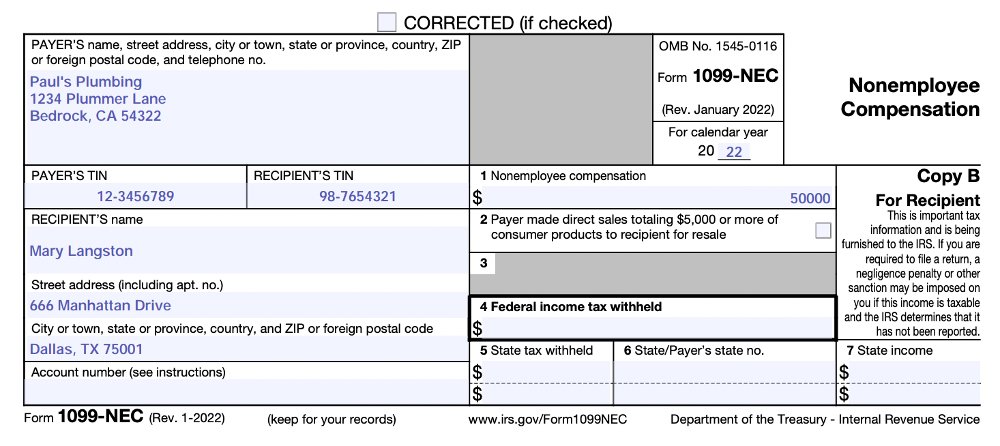

Here is what Form 1099-NEC looks like, along with a brief description of what type of payments are reported in each box:

Box 1. Nonemployee compensation

Report payments of $600 or more made to a nonemployee. Normally, you can report nonemployee compensation paid to individuals and partnerships.

Boxes 2 & 3. Direct sales totaling $5,000 or more of consumer products to recipient for resale

No information is required in this box, so leave it blank if it’s not relevant for you.

Box 4. Federal income tax withheld

Enter backup withholding. For example, persons who have not furnished their TINs to you are subject to withholding on payments required to be reported in box 1.

A contractor might be subject to backup withholding if, for example, they did not provide you with their federal taxpayer identification number or Social Security number. This is why it’s important to ask your contractors to give you a signed Form W-9 before paying them.

Boxes 5–7. State information

These boxes are provided for your convenience only and need not be completed for the IRS. Use the state information boxes to report payments for up to two states.

Keep the information for each state separated by the dash line. If you withheld state income tax on this payment, you may enter it in box 5. In box 6, enter the abbreviated name of the state and the payer’s state identification number. In box 7, you may enter the amount of the state payment.

Step 4: Provide Form 1099 to Independent Contractors & File With IRS

Provide one copy of Form 1099-NEC to each contractor or vendor and file all Forms 1099-NEC with the IRS. You will also have a copy you can send to your state tax department, if required. Send out these 1099 forms after you review them for accuracy and completeness.

Businesses hand-deliver, mail, or electronically send Form 1099-NEC to their contractors. When filing with the IRS, either mail in paper forms or electronically file them.

Form 1099-NEC Examples

We provide two examples of how to prepare Form 1099-NEC. Our first example is a 1099 for an outside consultant. In our second example, we describe a situation where a Form 1099-NEC is not required because the amount paid is less than the reporting threshold.

Mary is an independent human resources (HR) consultant. Your firm contracted Mary to set up your HR information system and provide training on the system. She is an independent contractor.

In 2022, your business paid Mary a total of $50,000 for nonemployee compensation. Since $50,000 exceeds the $600 threshold for nonemployee compensation, your business is required to file a Form 1099-NEC.

You show nonemployee compensation of $50,000 in Box 1. This means that Mary will have to claim $50,000 of taxable earnings on her tax return.

Below is a sample Form 1099-NEC that you would issue to Mary:

Chris is an independent QuickBooks ProAdvisor. Your firm hired Chris to set up your QuickBooks files and train you on how to use the system. Chris also reviews your financial statements every quarter to make sure that you are doing things correctly. Chris is an independent contractor.

In 2022, your business paid Chris a total of $599 of nonemployee compensation. Since $599 is less than the $600 threshold for nonemployee compensation, your business is not required to file a Form 1099-NEC for Chris.

Other Common 1099 Forms

There are several varieties of Form 1099. Form 1099-NEC is the most common for small and midsize businesses because this is the form used to report payments to independent contractors. However, before 2020, 1099-MISC was the most common.

Other varieties of Form 1099 for small and midsize businesses are:

- Form 1099-MISC:Issued by businesses to report miscellaneous nonemployee payments other than those to contractors, like those to attorneys, for rents, awards, etc.

- Form 1099-CAP:Issued by corporations to report changes in corporate control and capital structure

- Form 1099-DIV:Issued by corporations and financial institutions to report dividends paid to shareholders; C-corps may need to issue this form to their shareholders

- Form 1099-INT:Issued by businesses and financial institutions to report interest payments; businesses may need to use this form to report interest paid to individuals or partnerships

IRS Form 1099-MISC

Since Form 1099-MISC was the primary 1099 used by businesses before the 2020 changes, let’s go over when you would need to file it, along with the new instructions and layout.

2月28日提交的形式1099 - misc必须如果费尔e by mail and March 31 if you file electronically.

The minimum thresholds at which businesses are required to form 1099-MISC are:

|

Reason for Payment |

Minimum Amount Paid by Your Business |

|---|---|

|

Rents |

$600 |

|

Royalties |

$10 |

|

Prizes and awards |

$600 |

|

Withholding of federal income tax under the backup withholding rules |

Any Amount |

|

Fishing boat proceeds |

$600 |

|

Medical and healthcare payments |

$600 |

|

Direct sales of consumer products for resale anywhere other than retail stores |

$5,000 |

|

Substitute payments in lieu of dividends or interest |

$10 |

|

Crop insurance proceeds |

$600 |

|

Attorneys and lawyers |

$600 |

|

Cash payments for fish or other aquatic life |

$600 |

Box 1. Rents

Report all types of rent payments of $600 or more during the calendar year. This includes rent for office space, warehouse space, machines, or equipment.

Box 2. Royalties

Report total gross royalty payments of $10 or more during the calendar year. Royalties include payments to license intangible property like patents, copyrights, or trademarks. Royalties also include fees paid by a publisher to an author or literary agent.

Box 3. Other income

Report payments of $600 or more for prizes, awards, and certain other types of payments that do not fit into any other box on Form 1099-MISC.

Other types of payments reported in Box 3 include (seeInstructions for Form 1099-MISCfor details):

- Prizes and awards, including the fair market value of noncash items

- Payments made to a deceased employee

- Payments of Indian gaming profits to tribal members

- Payments for participating in a medical research study

- Termination payments to former self-employed insurance salespeople

- Punitive damages, damages for nonphysical injuries and illnesses

Box 4. Federal income tax withheld

Enter backup withholding in this box. If you withheld anyfederal taxfrom a nonemployee payment, you are required to file a Form 1099-MISC, even if the payment amount is less than the threshold.

Box 5. Fishing boat proceeds

Enter the individual’s share of all proceeds from the sale of a fishing catch in excess of $600. Also, report cash payments of up to $100 per trip that are contingent on a minimum catch and paid for other duties performed such as mate, engineer, or cook. Do not report any wages that belong on Form W-2.

Box 6. Medical and healthcare payments

Report payments of $600 or more made in the course of business to physicians, dentists, and other providers of medical or health care services. 1099-MISC forms with payments of this nature aren’t only sent to individuals and partnerships but also corporations and LLCs.

This box also includes payments from medical and health care insurers issued to health care providers. You are not required to include payments to pharmacies for prescription drugs.

Box 7. Payer made direct sales of $5,000 or more

Place a tick mark in box 7 if your business sold $5,000 or more of consumer products to an individual or partnership for resale in a nonretail environment. Typically, this is for Amway distributors and similar direct sales networks.

Box 8. Substitute payments in lieu of dividends or interest

报告支付10美元或更多的替代品payments in lieu of dividends or tax-exempt interest. Stockbrokers and financial institutions report substitute payments when dividends or tax-exempt interest is received on a security while those securities are on loan.

Box 9. Crop insurance proceeds

Insurance companies use Box 9 to report crop insurance proceeds of $600 or more paid to farmers. However, this amount does not need to be reported if farmers informed the insurance company that expenses have been capitalized for tax purposes.

Box 10. Gross proceeds paid to an attorney

Report payments of $600 or more made to an attorney or lawyer. These are reportable even if the amount is paid to a law firm organized as a corporation and even if the services were performed on someone else’s behalf.

Box 11. Fish purchased for resale

If you purchase fish for resale, you must report total cash payments of $600 or more made to people in the business of catching fish.

Box 12. Section 409A deferrals

In general, businesses do not have to complete Box 12. Section 409A refers to certain types of nonqualified deferred compensation plans. For more details, please refer to theInstructions for Form 1099-MISC.

Box 13. FATCA filing requirement

FATCA requires certain US taxpayers who hold foreign financial assets with an aggregate value of more than the reporting threshold (at least $50,000) to report information about those assets on Form 8938, which must be attached to the taxpayer’s annual income tax return.

Box 14. Excess golden parachute payments

Enter any excess golden parachute payments in this box. In general, an excess parachute payment is any amount that exceeds the average compensation for services in the individual’s gross income over the most recent five years. For more details, refer to theInstructions for Form 1099-MISC.

Box 15. Nonqualified deferred compensation

Report amounts deferred as part of a nonqualified deferred compensation plan that are includible in the taxable income of a nonemployee. Do not use this for deferred compensation for employees: that goes on Form W-2 instead. See the IRS’sInstructions for Form 1099-MISCfor more details.

Boxes 16–18. State information

These boxes need to be completed for those businesses that are required to file copies of Form 1099-MISC with state tax departments.

Bottom Line

Businesses may need to file Form 1099 to report various types of payments. If they paid $600 or more in compensation to contractors, freelancers, and other nonemployees, they must send copies of Form 1099-NEC to the IRS and the payees by Jan. 31 following the year in which the payments were made.

如果你需要帮助准备和发送1099形式to your independent contractors, consider using a payroll software like Gusto. For just $6 monthly per contractor, you can automate payments and tax form preparation (both W-9 and 1099 forms). And during the months you don’t need to pay your contractor, you won’t owe Gusto either. Sign up for a free trial today.