8 Best Virtual Terminals for Small Businesses in 2023

Meaghan has provided content and guidance for indie retailers as the editor for a number of retail publications and a speaker at trade shows. She is Fit Small Business’s authority onretailand ecommerce.

安娜是一个零售专家作家适合小普杜拉。布辛ess with over six years of evaluating dozens of software for small business. She holds a double degree in Accountancy and Financial Management and is currently pursuing further education in financial and payment technology.

This article is part of a larger series onPayments.

A virtual terminal lets store owners manually key in credit card numbers when they receive payment requests via phone, email, instant message, or mail. The best virtual terminals also let you send invoices and create recurring payments, making them good for billing.

Secure virtual terminals are available from almost any payment processor and require no special equipment. Transaction fees are higher than in-person transactions, though—it’s usually 3.5% plus 10 cents–15 cents per transaction.

The best virtual terminals are:

- Square Payments:Best overall

- Helcim:Best for storefronts

- Chase Payment Solutions:Best for B2B sales

- PayPal:Best for freelancers, occasional sellers, and cross-border sales

- Clover:Best for choosing your own merchant service

- Payment Depot:Cheapest option for established businesses

- PaymentCloud:Best for high-risk businesses

- Payline Data:Best for medical businesses, educational services, and nonprofits

Best Virtual Terminals Compared

|

Monthly Plan |

Virtual Terminal Fee (Monthly) |

Keyed-in Transaction Fee |

In-person Transaction Fee* |

Cross-border Fees** |

|

|---|---|---|---|---|---|

|

|

$0 |

$0 |

3.5% + 15 cents |

2.6% + 10 cents |

$0 |

|

|

$0 |

$0 |

Interchange plus 0.2% + 10 cents to 0.5% + 25 cents |

Interchange plus 0.1% + 5 cents to 0.3% + 8 cents |

$0 |

|

|

$0 |

$0 |

2.9% + 25 cents |

2.6% + 10 cents |

$0 |

|

|

$0–$30 |

$30 |

2.39% + 49美分至3.09% + 49美分 |

2.99% + 49 cents |

+1.5% |

|

|

$0–$44.95 |

$14.95/month |

3.5% + 10 cents

(Fiserv) |

2.3%–2.6% + 10 cents

(Fiserv) |

Depends on merchant account provider |

|

|

$79 |

$0 |

Interchange + 18 cents |

Interchange + 8 cents |

N/A |

|

|

$25–$30 |

$15–$45 |

2.7%–4.3% |

2.7%–4.3% |

Not disclosed |

|

|

$10–$20 |

$10 (one-time payment) |

Interchange plus 0.75% + 20 cents |

Interchange plus 0.4% +10 cents |

N/A |

*Merchants can link a card reader to their virtual terminal to take advantage of cheaper in-person rates when possible

** For merchants processing international payments requests sent over the phone or via email

Square Payments: Best Overall Virtual Terminal for Small Business

Pros

- Free to use, no monthly fees

- Free POS and invoicing features included

- Easy chargeback dispute procedures

Cons

- Locked into Square Payments

- Can only process B2B with integration

- Limited support forhigh-risk merchants

Square Payments Deciding Factors

- Built-in payment processing

- Free POS and Invoicing

- Next-day access to funds (Same-day with fee)

- Waived chargeback fees

- Add-on services like appointments or payroll

- CBD program for businesses selling CBD products

What We Like

方支付是内置的付款处理器for Square POS that’s great for small businesses, from startups to shops with a physical location and an online store—even restaurants and salons. The virtual terminal also comes free with every Square POS account that supports almost all payment methods (B2B payments processing requires third-party integration).

With 4.41 out of 5 in our review, Square topped our scores for feature set, checking off our full list of tools for handling one-time and recurring bills, managing customers and invoices, and taking payments. It’s easy to use on both web and mobile, although the limited customer support hours and limited ability to accept Level 2 and 3 payments brought down its overall score.

The downside to Square’s extensive feature set, especially for those businesses that do high-volume sales, is the transaction fee, which is the highest on our list. If you have consistent sales of over $5,000 per month, do a price comparison against Payline Data, Payment Depot, or Helcim, which offer interchange-plus pricing.

As you consider costs, however, keep in mind all the tools Square provides that you may otherwise have to pay for. As your business grows and you’re processing over $250,000 annually, you can apply for lower, custom rates through Square. Here are the standard fees:

- Monthly subscription fee:$0

- Virtual terminal monthly fee:$0

- Keyed-in (virtual terminal) transaction fees:3.5% + 15 cents

- In-person (swipe, dip, tap) transaction fees:2.6% + 10 cents

- Invoice transaction fees:3.3% + 30 cents

- 电子商务交易nsaction fees:2.9% + 10 cents

- ACH/bank transfer fees:1% with $1 minimum

|

Credit/debit cards |

Recurring billing |

|

ACH |

B2B payments (integration) |

|

Invoicing |

International payments |

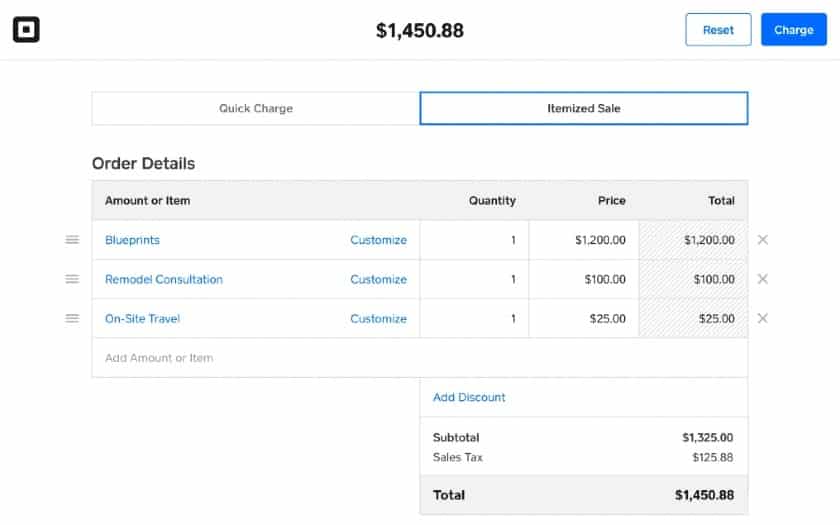

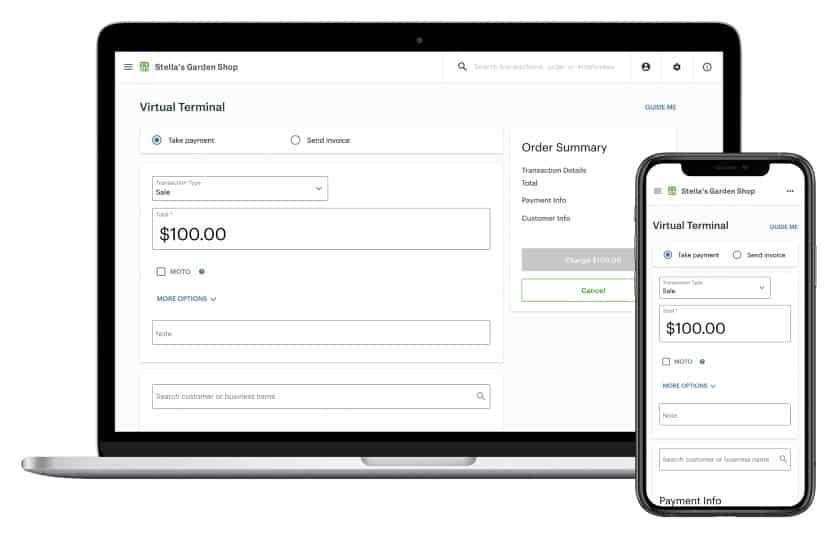

The virtual terminal includes inventory, recurring payments, and receipts. (Source: Square)

- Feature-rich payment tools:Square topped our scores for feature set, checking off our full list of tools for handling one-time and recurring bills, managing customers and invoices, and taking payments. It’s easy to use on both web and mobile, although the limited customer support hours and limited ability to acceptLevel 2 and 3 paymentsbrought down its overall score.

- 本地宝S integration:Square’s free POS software integrates with the virtual terminal, so you can itemize sales, calculate taxes, input discounts, and save customer information. Most of the other virtual terminals on our list are more basic, requiring you to manually input the items and prices unless you tie them to a POS system.

- Free virtual terminal:Like most Square products, the virtual terminal is free, easy to set up, and user-friendly. Your inventory gets automatically updated, and changes in your online store are also reflected in the virtual terminal. If you integrate with QuickBooks or other accounting software, the information from the virtual terminal is tied in as well.

Square also offers some of the best solutions forPOS software,merchant services,salon and spa software, andmobile payment processing.

Helcim: Best for Retailers & Storefronts

Pros

- Strong fraud protection

- Automated discounted interchange plus pricing

- No long-term contracts or monthly fees

Cons

- Lacks option for same-day funding

- Does not support high-risk merchants

- No inventory feature in virtual terminal

Helcim Deciding Factors

- Free virtual terminal

- Free POS

- Excellent rates

- ACH transactions

- Tokenized card information

- Lengthy merchant account approval process

What We Like

Helcim is on our list ofbest merchant servicesandleading retail credit card services. You will find other providers in our list that offer interchange-plus pricing; however, Helcim’s structure is a little different, with automatic volume discounts and no monthly fees.

As such, it’s a better choice for growing retailers with high-volume (but lower-ticket) sales because merchants do not need to apply for better rates as their transaction volume increases.

Earning 4.23 out of 5 on our evaluation, Helcim lost points for not catering to high-risk businesses (check PaymentCloud for that) and lack of 24/7 support. Nonetheless, Helcim earned high scores in all categories. The virtual terminal handles phone sales, invoices, and recurring payments. Like Payment Depot, Helcim also has a chargeback reimbursement program.

Helcim’s free monthly plan and automated volume discounts set it apart from the other payment processors on our list. Card-not-present transaction rates, including virtual terminals, range from Interchange plus 0.2% + 10 cents per transaction (if your sales average more than $5,000,000 a month) to 0.5% + 25 cents (for average sales of $2,500 and below a month).

This is considerably cheaper than Payline Data’s 0.75% + 20 cents, but more expensive than Payment Depot’s interchange + 18 cents (although note that you have to pay at least $59 in monthly fees). Domestic ACH transactions cost 0.5% + 25 cents.

|

Monthly Sales Volume |

Card-Present Rate

Interchange plus

|

Keyed and Online Rate

Interchange plus

|

|---|---|---|

|

$0–$25,000 |

0.3% + 8 cents |

0.50% + 25 cents |

|

$25,001–$50,000 |

0.25% + 7 cents |

0.45% + 20 cents |

|

$50,001–$100,000 |

0.20% + 7 cents |

0.40% + 20 cents |

|

$100,001–$250,000 |

0.18% + 6 cents |

0.35% + 15 cents |

|

$250,001–$1,000,000 |

0.15% + 6 cents |

0.30% + 15 cents |

|

$1,000,001–$5,000,000 |

0.12% + 5 cents |

0.25% + 10 cents |

|

$5,000,001+ |

0.10% + 5 cents |

0.20% + 10 cents |

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments |

|

Invoicing |

International payments (for merchants in Canada) |

Helcim lets you key in a card payment, or you can select the customer’s card stored in your Helcim card vault. (Source: Helcim)

- Stored-card payments:Helcim offers a simple virtual terminal that lets you put in credit card information. You can also store it to look up later. All the services on our list share this feature, but many of those we evaluated did not.

- Recurring payment processing:In addition to one-time sales, you can easily send invoices or set up recurring payments to automatically bill customers at a schedule of your choosing. Helcim’s virtual terminal can also be set up to accept multiple currencies.

- Highly-compatible virtual terminal platform:The virtual terminal also works on any device, making it a great tool for taking payments on the sales floor and at the register.

- Mobile app with the virtual terminal:You also get a mobile app and a free POS system that can work on your existing smartphone, iPad, or tablet. It accepts ACH payments—something you don’t find with some payment processors on our list, like PayPal.

Chase Payment Solutions: Best Virtual Terminal for B2B Sales

Pros

- Same-day and next-day funds possible

- Rates negotiable in some cases

- Direct processor—can use other payment gateways

- May accept international currencies

Cons

- Some services (Chase QuickAccept) limited to the US

- Some plans require long-term contracts

Chase Payment Solutions Deciding Factors

- Backed by trusted payment processor

- Offers advanced analytics tools

- Processes echecks

- Split payments, refunds, account histories

- Choose between Chase’ native virtual terminals, Orbital and Authorize.net.

- Also works with non-Chase deposit account holder

What We Like

We recommend Chase Payment Solutions for businesses that do B2B sales and those that need the support of an established bank, including checking, credit cards, and even loans. The system supports Level 2 and 3 data processing through its proprietary virtual terminal platform, Orbital.

Since our last update:

Chase has been aggressively building out its small business merchant services, which now support a wide range of payment processing methods, plus a unique and advanced analytics tool that comes free with every merchant account.

Chase climbs to the third spot on our list, also improving its overall score for this update, 4.04 out of 5, after points were adjusted to reflect B2B payments and the required checking account, which can cost anywhere from $0 to $15 per month (if you have a Chase business checking account that doesn’t meet the required $2,000 monthly minimum balance). It lost points for the chargeback fee of $25 to $100 (where Square, for example, waives it).

That said, Chase offers excellent features and is one of our top picks for thebest small business checking accounts. It also works with some high-risk businesses (while Helcim does not).

You don’t need to have a Chase Business Checking account to sign up for a merchant account with Chase. Those who do, however, have access to free same-day funding. Otherwise, merchant accounts are free to use, but the use of virtual terminals may cost extra (not disclosed).

事务率随平台,但对virtual terminals, they are 3.5% + 10 cents per keyed-in transaction, which is slightly less than Square’s keyed-in rate. Like PaymentCloud (and possibly Payline Data), there may be room to negotiate for better rates. Some influencing factors are sales volume and whether or not you process B2B sales, which are more secure and usually have lower rates.

- Monthly fee:$0

- 虚拟终端费:Not disclosed

- Online fee:2.9% + 25 cents

- In-person fee:2.6% + 10 cents

- Keyed-in fee:3.5% + 10 cents

- ACH processing:$25 per month for 25 transactions, 25 cents for each additional, or 1% for certain platforms

- Chargeback fee:$25–$100

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments (proprietary or third-party integration) |

|

Invoicing |

International payments |

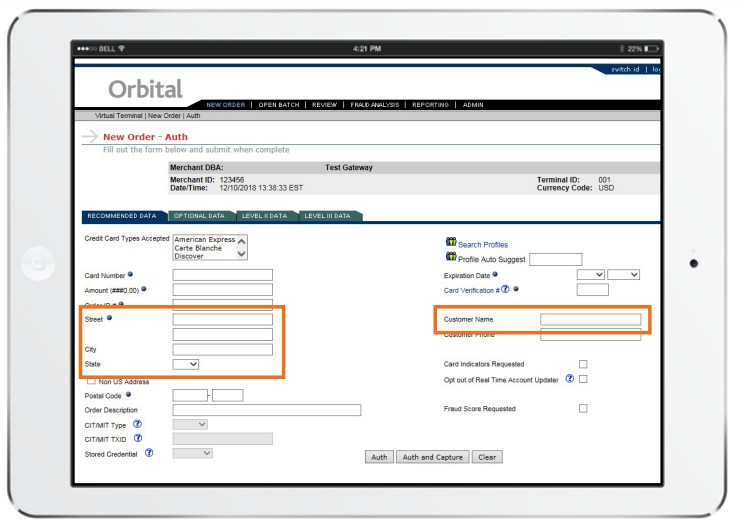

Chase’s Orbital Virtual Terminal lets you save customer data including card information to use again. (Source: Chase)

- Multiple virtual terminal options:Chase lets you have a choice of virtual terminals. If you prefer to use Authorize.net with Chase, you can start accepting payments over the phone. However, Chase has its own—Orbital Virtual Terminal.

- Native virtual terminal with shipping management:Orbital lets you process purchases and refunds and allows splitting of shipments, something we did not find in other virtual terminals, but which makes it well-suited for sales that might need a deposit.

- B2B payment processing:Unlike many virtual terminals on our list, Chase supports Level 2 and Level 3 card processing, which can get you better rates if you qualify. You may also be able to process international currencies and electronic checks like PayPal. All you need to do is discuss this when setting up your account.Learn more about B2B payment processing.

- Free same-day funding:With a Chase bank account, you can get your funds the same or next day. Square charges extra for this, while PayPal will send money immediately but only to your PayPal account.

PayPal: Best Virtual Terminal for Solopreneurs & Occasional Sellers

Pros

- Trusted name in online payments

- Seamless integration options

- Discounted virtual terminal fee for nonprofits

Cons

- Virtual terminal has a monthly fee

- Lacks Level 2/3 data processing for B2B

- Complex pricing structure

PayPal Deciding Factors

- Instant fund access through your PayPal Account

- Peer-to-peer payments

- Low flat-rate in-person transaction fee w/ PayPal Zettle

- Integrates with hundreds of POS and third-party payment systems

- Easy-to-use platform

What We Like

PayPal is by far the most recognized payment processor in the world with easy integrations that let you put a payment button just about anywhere. Its virtual terminals can process most types of payment methods, including cross-border transactions. The system is popular for solopreneurs, occasional sellers, and hobbyists who have low sales volume and would not mind the flat-rate payment processing fees.

For this update, we gave PayPal’s virtual terminal a score of 3.89 out of 5 with an advantage in international scope and its many integrations with other popular small business software. However, it’s a simpler tool, lacking inventory and POS like Square, although you will get these free with a regular PayPal Zettle account. The use of its virtual terminal will also cost you $30 a month.

That said PayPal is undeniably a trusted name in the payments industry and makes our lists formobile credit card processingandmerchant services.

贝宝不处理ACH paym大受欢迎ents and imposing additional fees for invoicing and recurring billing tools and chargeback protection. It charges $30 per month for use of the virtual terminal, which pales in comparison to Square as it offers similar tools (POS, payment processing) for free.

However, Square’s transaction rates are slightly higher, with PayPal offering 3.09% + 49 cents per transaction for standard virtual terminal rates. It also offers a discounted transaction fee of 2.39% + 49 cents for nonprofits.

- Monthly fee:$0–$30

- Standard card-present fee:2.99% + 49 cents

- Virtual Terminal fee:$30 per month plus

- Standard:3.09% + 49 cents

- Charity:2.39% + 49 cents

- Payment Gateway (Payflow):$0–$25/month

- Recurring Billing:$10 per month

- Invoicing:3.49% + 49 cents

- Chargeback Fee:$20

- Chargeback Protection:0.4%–0.6% per transaction

|

Credit/debit cards |

Recurring billing |

|

Echecks |

B2B payments |

|

Invoicing |

International payments |

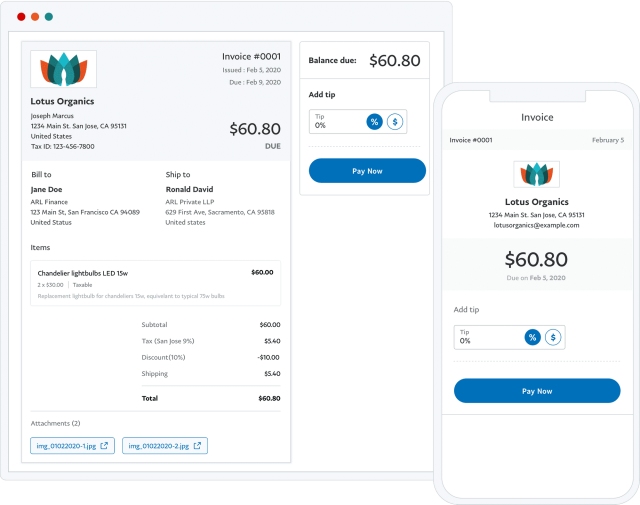

You can use PayPal’s virtual terminal to send invoices on desktop or mobile. (Source: PayPal)

- Free POS integrations:PayPal’s virtual terminal is a simple tool, but the system itself gives you access to a lot of free tools, such as the free POS software, Zettle, and its mobile app.

- Third-party integrations:The virtual terminal does not integrate with PayPal’s POS solution, limiting its ability for inventory tracking or itemizing sales. That said, you still have access to these tools through PayPal and a multitude of other third-party apps.

- International payment processing:One of PayPal’s strengths is its international reach—200 currencies, with international exchange. It also comes with an application that lets your customers make installment payments rather than paying in full. Combine all these with international payment processing, and you have a system that can take payments in any currency and through any venue.

Clover: Best Virtual Terminal for Choosing Your Own Merchant Service

Pros

- Works with a variety of merchant accounts

- $100,000 in liability protection in case of a data breach

- Easy to use

Cons

- Hardware tied to the merchant account

- Complicated pricing structure

- Requires Clover subscription

Clover Deciding Factors

- End-to-end encryption of virtual terminal payments

- Included with POS system

- Proprietary hardware

- Can be purchased from third party providers

- Choice of merchant providers

- Integrates with CRM

What We Like

Clover is a highly popular POS system because it’s offered by so many merchant services. As such, you can shop around for the payment processor that works best for your business. Its system comes with a free virtual terminal which you can subscribe to without the hardware at $14.95 a month. It provides you with Clover software, dashboard, and end-to-end encryption of all payments you accept over the phone, in person, or through an invoice.

For this update, Clover’s overall score slightly improved to 3.88 out of 5. It’s a feature-rich system and, with the right merchant service, extremely affordable. Clover lost points for requiring a monthly fee to access the virtual terminal feature, and for not monitoring its resellers, so you get a mix of great and terrible. However, the virtual terminal integrates with the POS system, handles invoices and recurring payments, and is generally easy to use. You will also find Clover on our list of thebest mobile payment processors.

Clover’s pricing is difficult to pin down because it has hundreds of resellers, many of whom offer discounted or even free Clover systems. The transaction rates similarly vary. When purchased directly through the Clover website, POS prices are from $0 to $44.95 per month, depending on your system, plus transaction fees of 3.5% + 15 cents for keyed-in transactions, which is on par with Square.

- Monthly Plan:

- Starter:$0 (Payments only)

- Standard:$14.95

- Advanced:$44.95

- Virtual Terminal (no hardware):$14.95/month, 3.5% + 10 cents keyed-in rate (Fiserv)

- Card-present fee:2.3%–2.6% + 10 cents (Fiserv)

- Default transaction rates and chargebacks by Fiserv but will vary by payment provider

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments |

|

Invoicing |

International payments |

You can subscribe to Clover’s virtual terminal instead of signing up for a hardware plan. (Source: Clover)

Like the other virtual terminals on our list, you can access Clover from any device over the web and process payments or refunds on the spot. It only processes credit or debit, unlike Square and Helcim, which handle ACH payments, or PayPal and Chase, which can accept echecks. You can also request payments via email and receive payments online.

Clover is unique in that you can use its virtual terminal with hundreds of different payment providers. (Chase and Payment Depot, on the other hand, require you to use them as a merchant service and select a virtual terminal.) Like PaymentCloud and Chase, Clover can integrate with some CRM software, such as Zoho.

Payment Depot by Stax: Cheapest Option for High-volume Sales

Pros

- Surcharging management tools via CardX

- All-in-one subscription

- Integrates with POS and ecommerce

- Has a free mobile app

Cons

- US-based merchants only

- Charges monthly fee

Payment Depot Deciding Factors

- Choice of virtual terminals through Authorize.net, SwipeSimple, NMI, and more

- Interchange-plus pricing

- Sales staff helps you find the best terminals and POS systems for your business

- Multiple integrations

- Free equipment reprogramming

What We Like

If you do high-volume sales, then a payment processor with interchange-plus pricing can save you hundreds to thousands of dollars, even when considering a monthly fee. Payment Depot is one of our top picks for thecheapest credit card processing companies, and that includes virtual payment terminals. While it does not work for high-risk businesses or businesses outside the US, it is worth considering for any business with high-ticket sales. It offers a choice of free third-party virtual terminals and makes our list for the strength of the payment processing.

Payment Depot earned 3.81 out of 5 in our evaluation. The virtual terminals generally don’t include inventory—check Square for that. Like most on this list, it loses points for not supporting high-risk businesses. It lost the most points for its steep monthly fee. However, chargeback protection is included in its membership price, and it fares well for ease of use, integrations, and reputation.

We’ve also liked Payment Depot for generalmerchant servicesandrestaurant payment processing.

The best thing about Payment Depot’s price is that there is no percentage markup. You only pay a flat fee of 8 cents to 18 cents per transaction, plus the interchange price that every processor charges. No other virtual terminal on our list does this. (Some, like Square, Chase, and PayPal, fold the interchange charge into their rates.)

If you process high-dollar-value transactions, you could save thousands of dollars. It also offers a calculator to help you determine how much you’re paying. Note, though, that Payment Depot now only has one subscription plan ($79) for merchants processing up to $21,000 per month. These are the highest monthly fees of any option on this list, but plans include a free virtual terminal and may also include equipment.

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments |

|

Invoicing |

International payments |

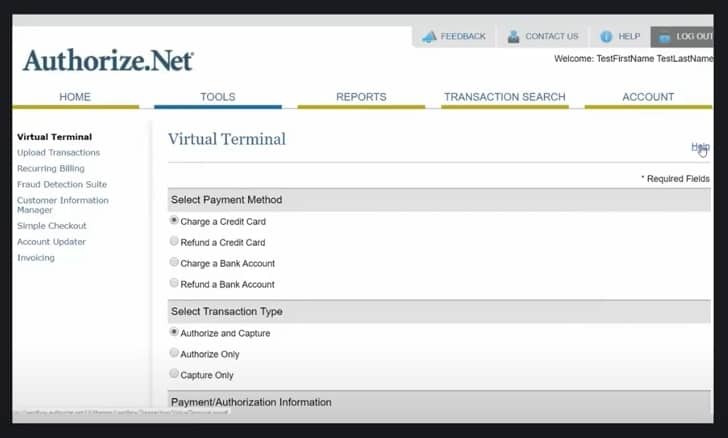

Payment Depot offers several virtual terminals, depending on the plan you purchase. Shown here: Authorize.net.

(Source: Authorize.net demo)

- Highly compatible with most virtual terminals:Unlike most of the products on this list, Payment Depot does not have its own virtual terminal, but gives you a choice of several such as Authorize.net, SwipeSimple, PayTrace, and NMI.

- B2B payments processing:While we prefer Chase Merchant Services for B2B sales, Payment Depot also offers credit card processing with Level 2 and 3 rates through PayTrace.

- Business management integrations:Payment Depot itself integrates with QuickBooks, POS systems, and other software. It also provides merchants with POS equipment reprogramming for free.

- Responsive customer support:We give Payment Depot kudos for customer support. I sent a question via the contact form and got a call minutes later. The support person was friendly, helpful, and did not try to hard-sell me anything. Other FSB reviewers have had similar experiences, and the user reviews also call out the great service.

PaymentCloud: Best Virtual Terminal for High-risk Businesses

Pros

- Specializes in high-risk businesses

- Flexible pricing structure

- Connects to inventory, CRM

- Strong fraud prevention tools

Cons

- Charges a gateway fee

- Minimum two-year contract

PaymentCloud Deciding Factors

- Supports multiple virtual terminal options

- Integrates with popular POS

- Supports invoices and recurring sales

- Flexible pricing structure

- Gateway agnostic

- Custom fraud protection

- Waived early termination fees

What We Like

While it can serve traditional merchants, PaymentCloud specializes in working withhigh-risk businessessuch as Mail Order Telephone Order (MOTO) that can highly benefit from a virtual terminal solution. It has relationships with over 10 banks that can handle high-risk customers and transaction rates are naturally steeper. But what’s unique with PaymentCloud is that it can adapt its fee structure (interchange-plus, flat rate, tiered) based on the merchant’s preference.

PaymentCloud earned an overall score of 3.78 out of 5, standing out for its ability to support all types of merchants and flexible fee structure. On the other hand, it lost points primarily because it charges fees for a number of its services including payment gateway integration and customization, monthly subscription, and chargebacks.

PaymentCloud is the only virtual terminal provider on our list that does not have any publicly disclosed pricing. However, this does not come as a surprise—most high-risk merchant account providers do not disclose pricing because rates are customized to each business.

快速与PaymentCloud代表的电话,however, gave us an overview of typical rates:

- Monthly fee:$10–$45

- Virtual terminal:$15–$45 per month

- Medium-risk transaction fee:2.3%–3.4%

- High-risk transaction fee:2.7%–4.3%

- Payment gateway fee:$15 per month (average)

- Chargeback fee:$25

- Early termination fee:Waived

It negotiates with its partner banks to get you the best rates it can, and even adjusts its fee structure to match your needs; plus, it does not charge application, setup, or annual fees.

Aside from credit cards, PaymentCloud also accepts electronic check payments and credit and debit cards (like PayPal and Chase). Some of the virtual terminals on our list, like Square and Helcim, process ACH transfers instead.

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments |

|

Invoicing |

International payments |

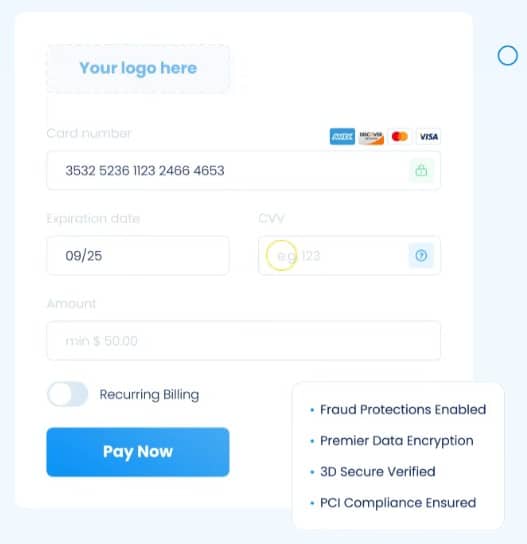

PaymentCloud includes recurring billing and invoicing. (Source: PaymentCloud)

- Advanced payment security tools:Advanced security is one key feature of PaymentCloud’s virtual terminals. It provides PCI compliance, fraud protection, data encryption, and multiple security verifications such as Visa 3D Secure, Mastercard SecureCode, JCB International J/Secure, and American Express SafeKey.

- Simple invoicing features:PaymentCloud can process credit card information but does not let you ring up itemized sales. You can use it to send and accept invoice payments, set up recurring transactions, and send digital receipts.

- CRM integrations:The platform is also specifically designed to connect with CRM software like Salesforce, unlike most providers in our roundup.

- Requires application and approval process:Note that the signup process can take longer than other virtual terminals, such as Square or PayPal, which are sign-up-and-go, but that’s because of the nature of being a high-risk business. However, you can be assured that PaymentCloud will assist you through the application process to make sure you have all the documents needed to get approved by one of its partner banks.

Payline Data: Best Virtual Terminal for Medical, Nonprofit & Educational Services

Pros

- Includes mobile app, in-person payment processing

- No chargeback fees

- First month is free

Cons

- Required $25 minimum transaction

- One-time $10 fee for virtual terminal

- Pricing structure can be confusing

Payline Data Deciding Factors

- Health Insurance Portability and Accountability Act (HIPAA)-compliant tools

- Verifi Cardholder Dispute tools

- Special rates for certain industries

- Recurring payments, invoicing

- Charges a one-time fee for use of virtual terminal

What We Like

Payline Data services a wide range of businesses but has a particular focus on the medical industry, with HIPAA-compliant tools, ACH transfer, and special pricing. It also has special considerations for nonprofit and educational services. Payline Data merchants get access to its virtual terminal application with a one-time $10 fee and works as well as most and can handle invoices and recurring payments.

All things considered, Payline Data earned an overall score of 3.68 out of 5. Though slightly lower than the previous update, it earns much of its score on the strength of Payline as a payment processor. Payline Data stands out for its compatible features for nonprofit, medical, and educational institutions, while also offering interchange-plus pricing, which makes it a better deal than most for high-volume businesses.

Payline has a monthly fee (with a one-month free trial) and, in return, offers low interchange-plus pricing. The fees run $20 for online transactions and $10 for in-person transactions. The virtual terminal has a one-time fee of $10, after which it costs nothing.

For online and virtual terminal sales, it charges interchange + 0.75% + 20 cents. Compare this to Payment Depot, which has only an 8 cents to 18 cents transaction fee but a higher monthly membership.

Payline stands out from the rest, however, in its special pricing for medical facilities, nonprofit organizations, and educational institutions.

- Transaction fee for medical:Interchange + 0.2% + 10 cents

- Transaction fee for nonprofit, educational:Interchange + 0.1% + 10 cents

The Payline Data website says it provides payment processing for high-risk businesses adding a 0.1% per transaction fee; however, according to a Payline rep, it actually refers high-risk merchants to PaymentCloud, which is on this list.

|

Credit/debit cards |

Recurring billing |

|

ACH/echecks |

B2B payments |

|

Invoicing |

International payments |

The Payline virtual terminal can be accessed on the web or mobile.

(Source: Payline Data)

- HIPAA compliance:Payline Data services a wide range of businesses but has a particular focus on the medical industry, with HIPAA-compliant tools, ACH transfer, and special pricing. It also has special considerations for nonprofit and educational services

- Multiple virtual terminal options:Payline Data offers a credit card virtual terminal through CardPointe, NMI, Transax, and Authorize.net. All provide tokenization andPCI compliance. Some offer customer management and allow for subscriptions, recurring payments, and electronic invoicing.

- Nonprofit payments processing:As a HIPAA-compliant payment processor, Payline is equipped to protect patient data, something we did not see in other virtual terminal software. Nonprofits and educational services can benefit from the ACH transfer capability.

- Fraud and chargeback protection:Payline Data also comes with strong fraud and chargeback protection (through Verifi). In addition to data to help you discover fraudulent transactions, it alerts you to chargebacks faster and gives you 72 hours to resolve the dispute before it becomes a chargeback.

Calculate Your Estimated Virtual Terminal Fees

Find out how much you would pay in monthly merchant payment processing fees with our recommended providers.

Guide:这个计算器假定您使用的是一个古董al terminal on your laptop/desktop computer with a card reader to accept payments. Please indicate below your estimated monthly sales volume for card-present transactions (payments using a card reader) and card-not-present transactions (payments accepted online and over the phone).

Looking for other ways to remotely accept payments?

Check out our list ofbest payment gatewaysandleading mobile point-of-sale applications.

How We Evaluated Virtual Terminals

We’ve looked at dozens of payment processors that offered virtual terminals and narrowed them down. All of our picks also include invoicing and recurring payment tools. From there, we took a close look at the pricing, toolset, and ease of use to come up with a list that offers the best value for the price while being easy for most managers and employees to work day by day.

We found Square to be the best virtual terminal credit card processing for small merchants with simple, competitive pricing and excellent sales and inventory features. Its fees are higher than interchange-plus companies like Helcim, but it offers free tools that can grow with your business.

Click through the tabs below for our full evaluation criteria:

30% of Overall Score

We awarded premium points for providers that offer low transaction fees. In addition, we also considered additional charges for accessing the terminal, chargeback fees, and merchant accounts. Helcim and Square lead this category with 4.5 out of 5.

25% of Overall Score

These cover payment types, recurring billing, inventory and customer management, and B2Bs. Helcim received a perfect score for this category, while Square, PayPal, Chase, and Clover come in second.

25% of Overall Score

We looked for fast deposit speed, dispute management, and in-person payments. We also considered when customer service was available.Chase did well in this category, only missing points for supporting high-risk businesses.

20% of Overall Score

This score takes into account usability as a whole, from affordability to stability of the software, account freezes, processing limits, and whether it integrates with other applications. We also considered input from real-world users. All of the providers did well here, but Square received a perfect score.

How to Choose a Virtual Terminal

Like most payment methods, it’s important to find virtual terminals that complement your business model and give you the most value for your money. Consider the following questions.

Some processors will charge a monthly fee for virtual terminal software. However, thebest merchant accountsoffer virtual terminals for free, so you just pay a processing fee with each transaction. The top providers in our list offer free access to its virtual terminal.

Note however, that this is different from the monthly account maintenance fee which can also be free depending on your payment processor.

Transaction rates vary depending on your sales volume and you will need to identify how much sales you process each month to get the maximum savings. For virtual terminal transactions, keyed-in rates, which are higher, are most often used.

- Providers with flat rate fees like Square will be more cost-effective to occasional sellers or to businesses with less than $10,000 in monthly sales.

- Merchants that process large volumes of sales per month will save more with providers offering interchange-plus rates like Helcim.

The best virtual terminal credit card processing should be able to process different payment methods that match your business model. Different modes of payment also carry different transaction rates that you should compare before choosing a virtual terminal. Payment methods available in virtual terminals are:

- Keyed-in credit card payments: The most popular method in virtual terminals. Transaction rates for this payment method is usually more than 3%.

- Tap, dip, swipe: This is possible with certain payment services providers that allows merchants to connect a credit card reader on their computer. It’s popular with warehouse-type, bulk-sale, business setup, especially since the transaction rates are lower (2.2% to 2.9%).

- ACH payments: This payment method allows merchants to request payment directly from a customer’s bank. The rates are much lower (around 1% per transaction) because it does not carry additional fees from card networks. However, for this payment method, it’s important to ask for the deposit speed.

- International payments: Some providers support multicurrency and/or currency conversion. This allows merchants to accept payments from international customers using the virtual terminal. Note that this carries an additional fee imposed by card networks and (sometimes) by the payment services providers.

- Level 2 and Level 3 data processing for B2Bs: This type of payment method offers secure payment processing and significantly lower rates for high-volume businesses. It will require additional customer information to be entered in the virtual terminal. Make sure to compare rates.

Most transactions processed through a virtual terminal come from an invoice sent to customers via email (sometimes even a text message). While there is also a payment button within the invoice, some customers prefer to send an email back with their payment information or call to process their payments over the phone.

Look for invoicing software that offers:

- Free use (with optional paid plan for advanced tools)

- Ability to create invoice templates

- 定制发票信息的能力

- Ability to set up recurring billing

- Ability to add custom branding

- Ability to track and follow up outstanding invoices

All payment processors and merchant services providers ensure that merchants and the software itself comply withPCI security standardsespecially for keyed-in transactions. However, the level of security among providers is not the same so you need to:

- Confirm that your provider’s virtual terminal is PCI compliant

- 问什么样的身份验证方法(address verification, CVV, etc.)

- Ask if fraud detection tools can be customized

- Ask if there are fees involved in using their fraud detection tools

Best Virtual Terminal Frequently Asked Questions (FAQs)

A virtual credit card terminal offers several payment processing conveniences. It does not require specialized hardware and is accessible through a web-based platform (computer or mobile device). Additionally, it is secure and PCI-compliant. A virtual terminal can accept all types of payment methods, including invoicing, and can integrate with shopping cards, websites, and CRMs.

If you often accept payments online, over the phone, or via email, and prefer not to invest in additional hardware, then a virtual terminal may be your best option.

Virtual terminal transaction fees are higher than in-person transactions, though—it’s usually 3.5% plus 10 cents–15 cents per transaction. Also, some processors will charge a monthly fee for virtual terminal software (different from the monthly account maintenance fee). However, the best merchant accounts offer virtual terminals for free, so you just pay a processing fee.

Yes, all built-in virtual terminals in our list observe PCI compliance for accepting online payments as well as payments over the phone. Credit card information is encrypted as soon as it is encoded on the virtual terminal and the system ensures that none of the keyed-in data is saved.

Here is how payments are completed through a virtual terminal:

1) Customer calls over the phone, sends an email, or contacts through instant messaging; 2) Merchant accesses customer’s invoice from the dashboard to set up payment; 3) Merchant keys in customer’s payment information for the invoice; 4) The payment processor encrypts the payment details and gets real-time approval to complete the transaction; 5) The merchant sends a digital receipt to the customer to confirm the payment.

Some virtual terminals are equipped with multicurrency and/or currency conversion. If your provider accepts international payments online, it’s likely that it can also accept the same on the virtual terminal. Note, however, that some impose additional fees on top of the cross-border fee passed on by the card network.

Bottom Line

Virtual credit card terminals are a great addition to any business, allowing you to take orders over the phone or by email. Most payment processors offer these for free or with a small monthly fee. The best handle multiple payment types, including cryptocurrency and ACH transfers, and have some form of fraud or chargeback protection that goes beyond PCI compliance.

Overall for small businesses, we find Square offers the best virtual terminal in the industry. It provides reasonable rates, has a free POS system, and is super easy to use. Plus, its wide range of products, includingpayroll processing, makes it a solid choice for growing businesses. Best yet—it’s free to use! You only pay a by-transaction rate. Sign up for Square today.